Analytical review by Halyk Research for February 2026 states that the high profitability of Kazakh banks is explained by temporary macroeconomic conditions and is not a sign of excessive profit. However, data from the review itself, as well as publications from the National Bank of Kazakhstan (NBK) and the Agency for Regulation and Development of the Financial Market (ARDFM), paint a more complex picture - with profit concentration, rising non-performing loans, and systemic constraints on competition.

WHAT HAPPENED: REVIEW AND REGULATOR'S RESPONSE

In February 2026, Halyk Research - the analytical department of the JSC 'Halyk Bank of Kazakhstan' structure - published a 'Review of Banking Sector Development (2018–2025): Imbalance in the Dynamics of the Retail and Corporate Sectors'. The central thesis of the document is that sector profitability 'is not evidence of excessive profitability', and competition 'precludes the formation of excess profits'.

Simultaneously, the ARDFM published two documents with different emphases. The first - results of the regular Asset Quality Review (AQR) for 2025. The second - supervisory priorities for 2026, providing for the introduction of a sectoral countercyclical capital buffer and a new prudential standard for consumer loan quality. The NBK, for its part, published an analytical note NBRK–AN–2025–03 with a detailed breakdown of retail portfolio quality by segment.

PROFITABILITY: FIGURES IN AN INTERNATIONAL CONTEXT

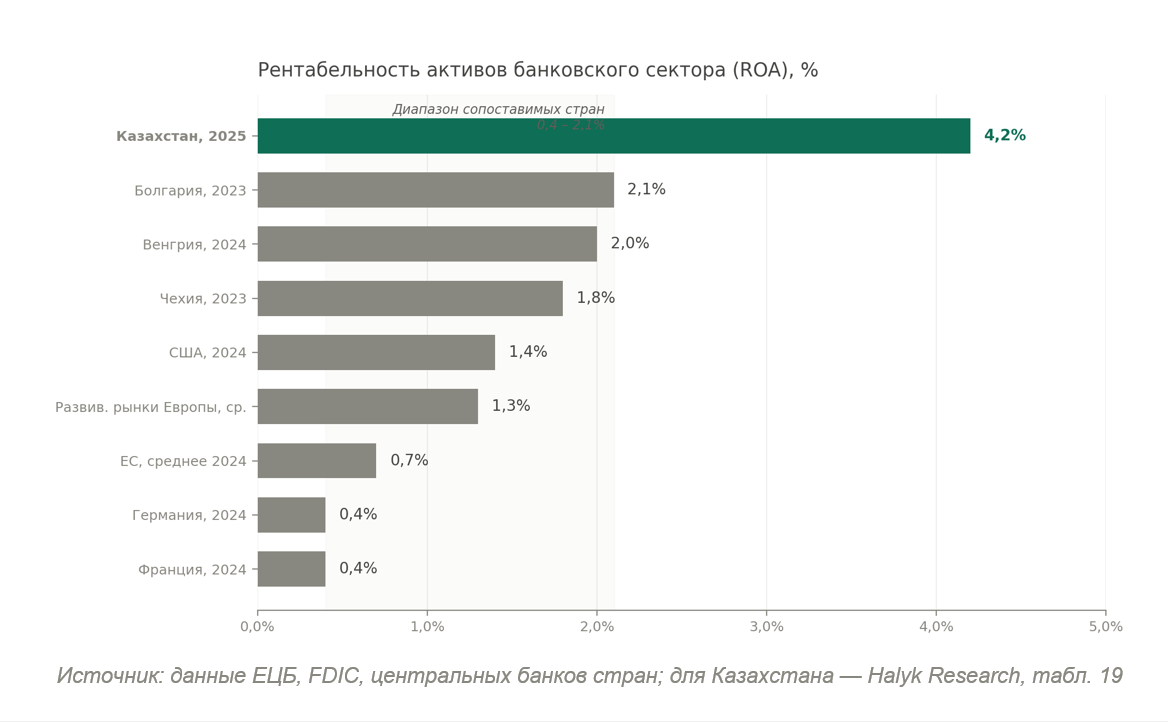

According to the Halyk Research review, the return on assets (ROA) of the Kazakh banking sector for 2025 stood at 4.2%. For comparison: the average ROA for US commercial banks is about 1.4%, and the average European figure is around 0.7%. Even the most profitable banking systems in Europe did not exceed 2.1% in the comparable period.

The authors of the review explain the discrepancy by the need to adjust for the level of inflation and the rate of tenge devaluation. The argument is methodologically debatable: the international ROA figures on which the review itself relies are calculated without similar normalisation. Applying an adjustment only to the Kazakh figure undermines comparability.

CONCENTRATION: TWO BANKS - MORE THAN HALF THE PROFITS

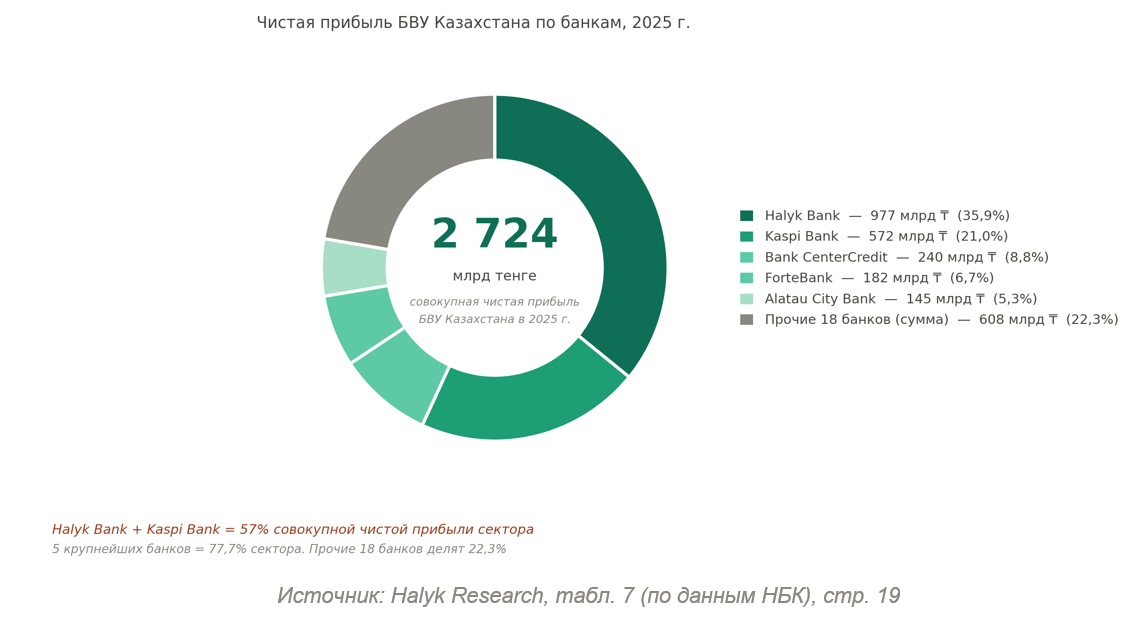

Data from the review itself allows for the calculation of the sector's profit structure. For 2025, the total net profit of the banking sector amounted to 2,724 billion tenge. Halyk Bank of Kazakhstan accounted for 977 billion tenge (36%), and Kaspi Bank for 572 billion (21%). In total, two banks provided 57% of the entire sector's profit, and the five largest provided 77.7%.

At the same time, Halyk Bank's profit exceeds the combined result of the other 18 banks by 1.6 times (977 billion tenge versus 608 billion).

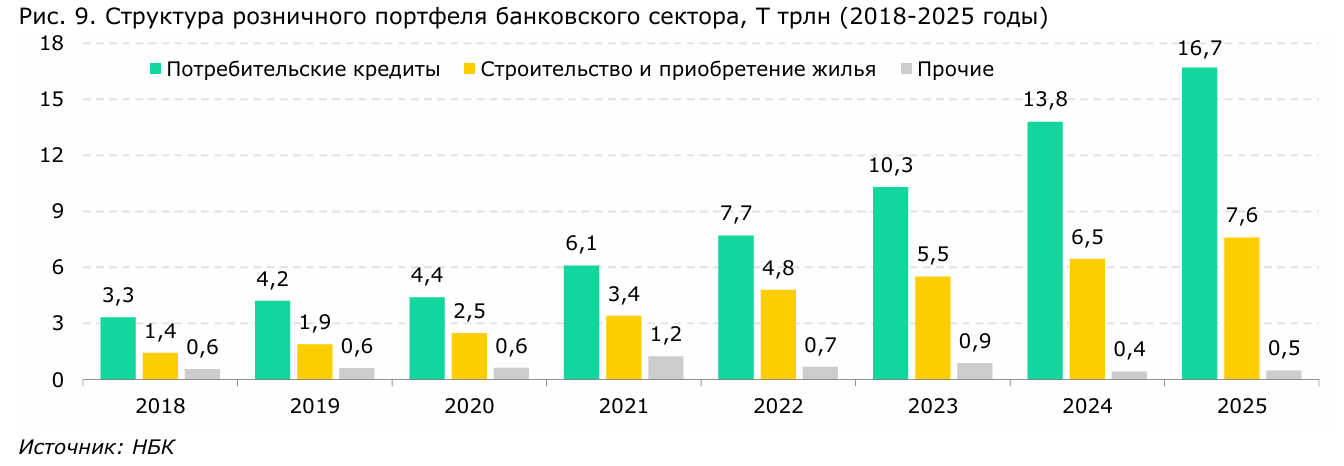

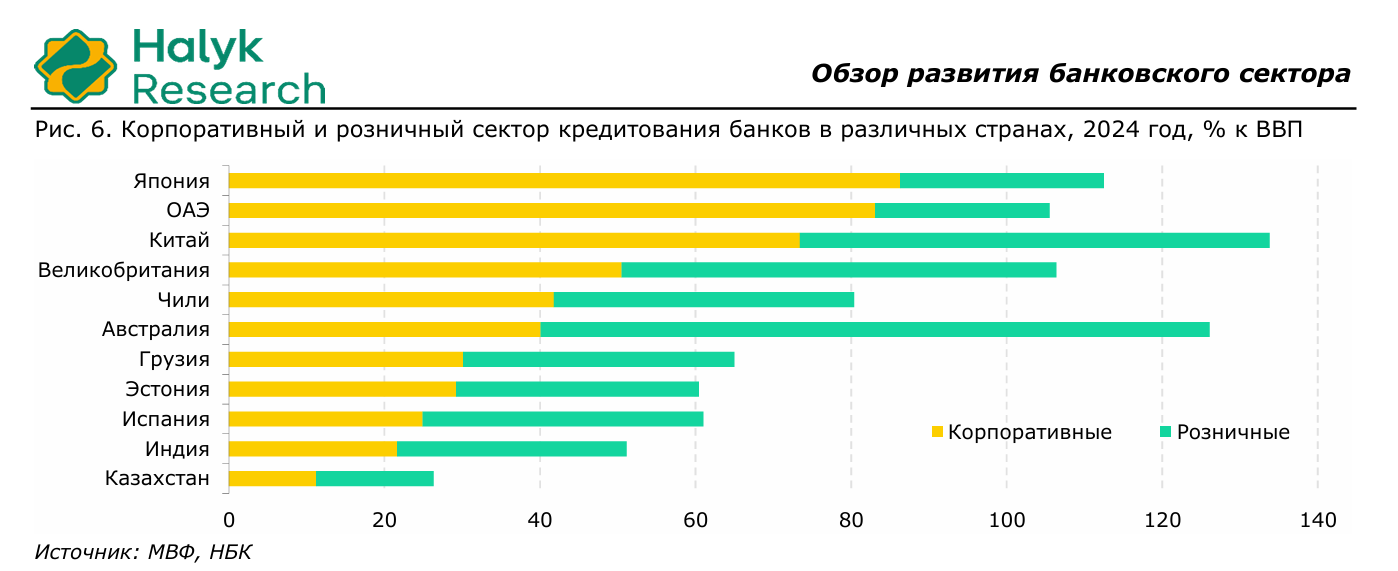

The review characterises the concentration of retail lending as 'low', pointing out that the three largest banks hold 60% of the retail portfolio. However, the NBK's analytical note provides Herfindahl-Hirschman Indices (HHI) for sub-portfolios: the mortgage market - 3501, unsecured consumer loans - 2560, secured consumer loans - 2462. Values above 1800 are interpreted as a sign of a highly concentrated market. Three out of four retail segments exceed this threshold.

PORTFOLIO QUALITY: THE AVERAGE FIGURE MASKING DISPERSION

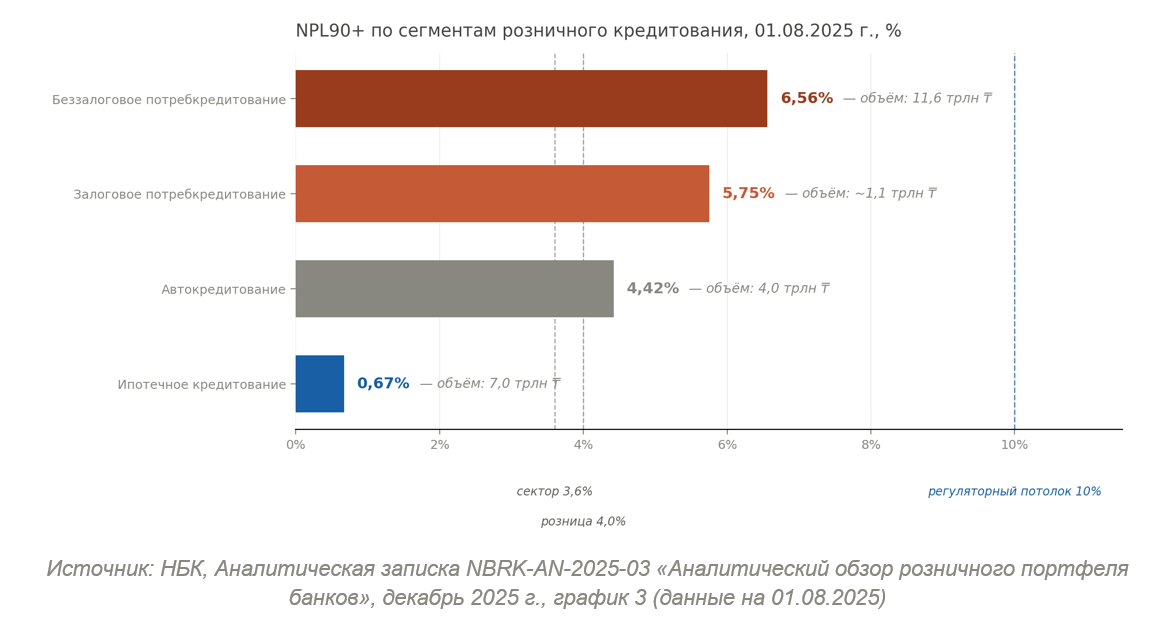

The Halyk Research review records the share of non-performing loans overdue by more than 90 days (NPL90+) for the sector at 3.6% at the end of 2025 - and characterises portfolio quality as 'relatively high'.

The NBK note breaks down this indicator by segment: mortgages - 0.67%, unsecured consumer loans - 6.56%, secured consumer loans - 5.75%, car loans - 4.42%. Unsecured consumer lending - the largest single segment of the retail portfolio - demonstrates an overdue rate almost ten times higher than mortgages.

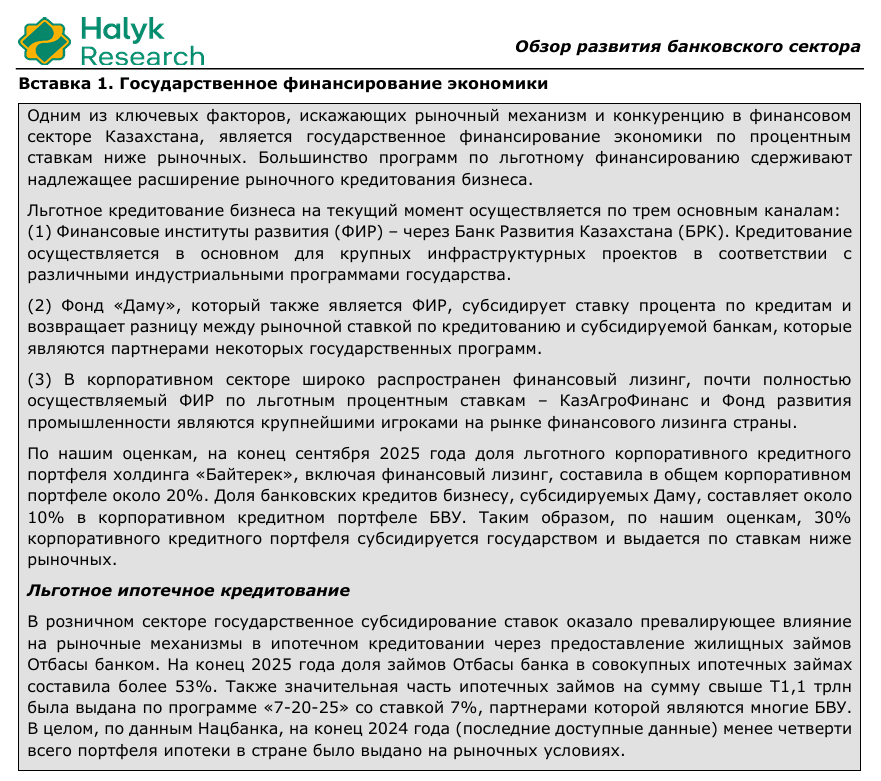

The low mortgage NPL is largely underpinned by government subsidies: according to the review, over 53% of the mortgage portfolio was issued through Otbasy Bank under preferential programmes, and another over 1.1 trillion tenge through the '7–20–25' programme with a 7% interest rate. The credit risk of these loans is effectively assumed by the budget, not by commercial banks.

Furthermore, the AQR–2025 results recorded a discrepancy between bank and regulator reserve estimates amounting to 377.4 billion tenge - predominantly for unsecured consumer loans and car loans. According to ARDFM estimates, banks are provisioning less than required by the independent supervisory assessment.

DEBT BURDEN: DEBT-TO-GDP RATIO IS NOT THE ONLY CRITERION

The review cites the ratio of retail lending to GDP as 16% and compares it with Chile (42%), concluding that values are 'moderate'. At the same time, the document itself notes that at the end of 2025, over 90% of Kazakhstan's economically active population had active loans, and the growth in household debt burden is outpacing the growth in their real incomes.

The debt-to-GDP ratio and the debt service-to-income ratio for a specific family are different parameters. The weighted average interest rate on consumer loans in Kazakhstan at the end of 2025 was 21.1%. A high nominal rate with a smaller absolute debt can create a higher burden on a household than in countries with lower rates but higher levels of debt.

An additional factor is the widespread use of interest-free instalment plans. According to the NBK note, as of 01.08.2025, 63% of retail borrowers were using them. The cost of these instruments is built into the commission fees of trading platforms and is not directly reflected in banking statistics on debt burden.

REGULATORY RESPONSE

Against the backdrop of the published reviews, the ARDFM announced the introduction, from April 2026, of a sectoral countercyclical capital buffer of 2% for retail lending, as well as a new standard - the consumer loan quality coefficient with a limit of 10%. According to the ARDFM's supervisory policy for 2026, based on SREP–2025 results, 7 out of 21 banks reviewed were categorised as 'moderately high' or 'high' risk.

In parallel, the corporate income tax rate for banks was increased from 20% to 25%, and higher minimum reserve requirements (MRR) were introduced. According to the Halyk Bank report for the first quarter of 2026, the bank's net profit decreased by 14.6% compared to the same period last year, partly due to the entry into force on 1 January 2026 of the new Tax Code, under which a number of banking services are subject to VAT at a rate of 16%.

SYSTEMIC CONTEXT: COMPETITION AND SUBSIDISED PROGRAMMES

The Halyk Research review details the issue of government-subsidised lending as a constraint on market-based bank financing. According to the authors' estimates, about 30% of the corporate loan portfolio is subsidised by the state. In mortgages, less than a quarter of the portfolio was issued on market terms.

At the same time, the authors simultaneously assert that competition in the banking sector precludes the formation of excess profits. Both theses appear in the same document without any attempt to reconcile them: if a significant part of the market is closed to market pricing, assessing the competitiveness of the remaining part requires separate justification.

EDITORIAL OPINION

The Halyk Research review is a detailed analytical document with an extensive factual basis. However, a number of key conclusions - regarding the absence of excessive profitability, a sufficient level of competition, and a moderate household debt burden - do not fully follow from the data that the document itself provides.

The discrepancy between these conclusions and the simultaneously published decisions by the regulator to introduce new capital buffers, supervisory standards, and the identification of under-provisioning amounting to 377.4 billion tenge - is not an editorial interpretation, but an observable fact. A substantive discussion on the state of the banking sector requires that these discrepancies be explicitly acknowledged, rather than remaining outside the scope of public debate.

CONCLUSION

The banking sector of Kazakhstan ended 2025 with high nominal indicators of profit and capitalisation. However, behind the aggregate figures lies a segmented picture: income concentration among the two largest players, rising overdue loans in unsecured consumer lending, a divergence in reserve estimates with the regulator, and the systemic presence of the state in pricing. The open question is how sustainable the current configuration of the sector will be when the base rate declines and interest margins shrink, which the review's own authors consider inevitable.